Jan 31, 2025

In this guide, we will walk you through the process of swapping or exchanging your...

![]()

.png?width=552&height=107&name=Image%202%20(2).png)

When you’re shopping for a new car, it can feel overwhelming trying to figure out which is the best type of car finance for you. With so many different kinds of contracts available and so much information out there online, it can be really difficult to do a fair comparison.

In this article, we’re going to take a look at 2 of the most popular forms of car finance available, Personal Contract Purchase (PCP) and Leasing, and how the costs compare to a car subscription. We’ll explain how each one works, what can be good and bad about them, and then do some cost comparisons with real-life examples, to look at the total cost of ownership over a set term. You might be surprised by the results!

PCP

PCP, or Personal Contract Purchase, is undoubtedly the most popular method of car financing in the UK. It's widely available at car dealerships and car supermarkets, often making it the first choice for those looking to finance a new set of wheels.

Typically lasting for 3 or 4 years, a PCP agreement requires a hefty deposit to secure a lower monthly cost. In a PCP agreement, you essentially pay for the car's depreciation while you own it, factoring in elements like your estimated annual mileage, the duration of the contract, and the projected market value of the car at the end of the contract (known as Guaranteed Future Market Value).

You’ll also be paying interest on the credit provided for the agreement, unless you bag a 0% APR deal which is becoming rare in the current financial climate.

When the agreement period comes to an end, you have three choices. First, you can simply return the car. Second, you can pay the balloon payment (the remaining value of the car) and the car becomes yours. Third, if you've accumulated any equity on the vehicle via overpayments, you can use it as a deposit for a new PCP contract.

Benefits of PCP:

Drawbacks of PCP:

Leasing

Leasing is much simpler than PCP car finance. Think of leasing as a long-term car rental, where you pay your monthly payments and then just give the car back at the end of the contract.

You need to put down an initial deposit but it’s usually much lower than the deposits required on a PCP contract. You usually choose either 3, 6 or 9 months worth of payments to put down as your initial deposit, depending on how much cash you have spare, and obviously the higher your initial deposit, the lower the monthly costs.

Just like with PCP, your monthly payments will be covering the cost of depreciation of the vehicle and the cost of credit. However, with a Lease contract you don’t build up any equity in the vehicle like you do with a PCP agreement.

And at the end of the lease agreement, you give the car back to the leasing company. So it’s simpler than PCP but you don’t have different options or the ability to negotiate with your dealer on a new deal.

Benefits of Leasing:

Drawbacks of Leasing:

Subscription

Here at Wagonex, we see car subscription as the future of car ownership, inspired by online services like Netflix and Amazon Prime it’s designed to meet changing consumer demand for convenience, flexibility and transparency. Subscription is set to shake up the car industry, but how is it different from leasing or PCP finance?

What sets Subscription apart is that all the costs for owning a car are included in one monthly payment. That includes the cost of the car, road-tax, maintenance, servicing, road-side assistance. It’s perfect if you don’t want the headache of arranging and managing all those other essential costs.

Plus, that one transparent, monthly subscription cost makes it so much easier for you to make an informed decision whilst shopping for cars. There are no hidden or unforeseen costs you need to go and work out.

With Subscription you choose how long you want the car for. You don’t have to be locked into a 3 or 4 year contract like a PCP or Lease contract. Instead, you can choose a 12 month, 6 month or even a 1 month subscription. It’s unrivalled flexibility, that also lets you try out different cars or adjust quickly to changes in your circumstances.

Ordering a car on Subscription is super convenient too. You pick the car you want and how long you want it for online, provide some details at the checkout and arrange the delivery.

And when your subscription is over, you just give the car back and move on. Nice and easy.

Benefits of Subscription:

Drawbacks of Subscription:

Comparing the total cost of ownership

Now after going through each of the 3 most popular types of car finance, you’ll probably have a better idea of what contract might work best for you and your situation. But seeing as cost is probably the most important factor, let’s take a more in-depth look at cost of ownership.

Earlier we saw that Subscription’s main downside was the higher monthly costs, compared to PCP and Leasing. But, is Subscription actually more expensive, when you factor in all of the costs over the whole term?

Let’s have a look at some real-life examples and do some thorough comparisons.

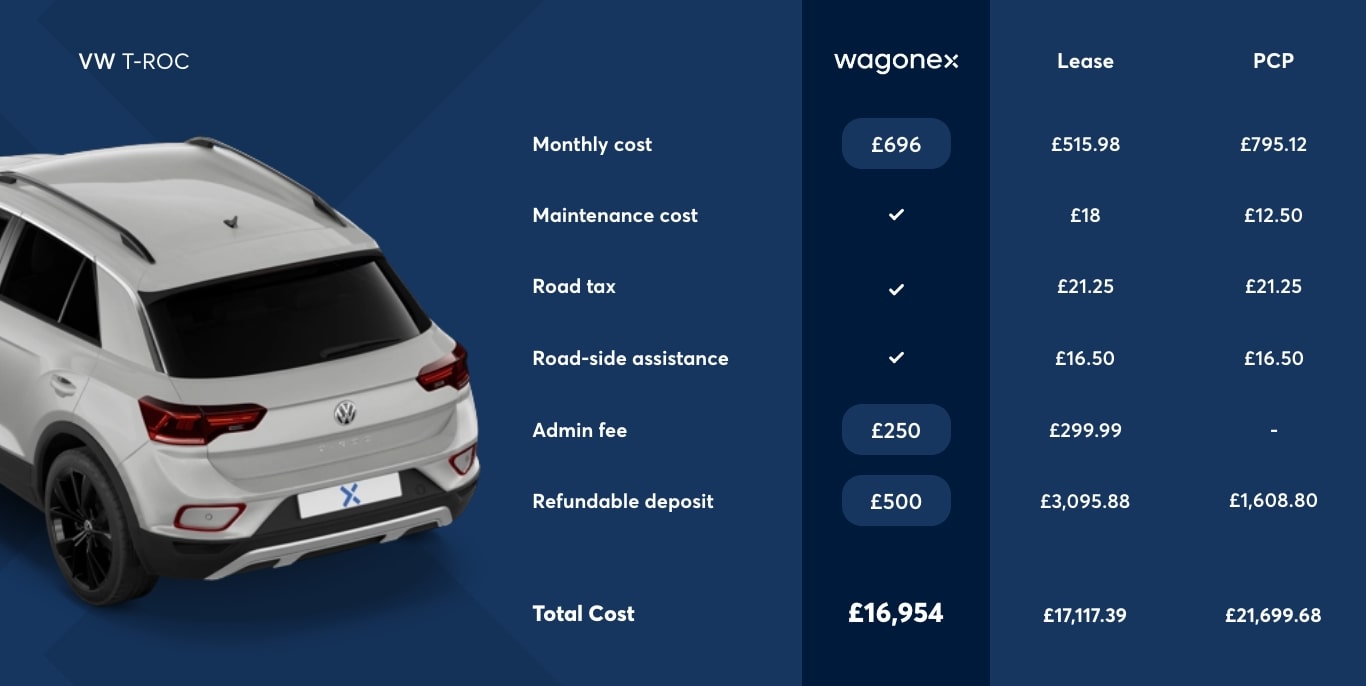

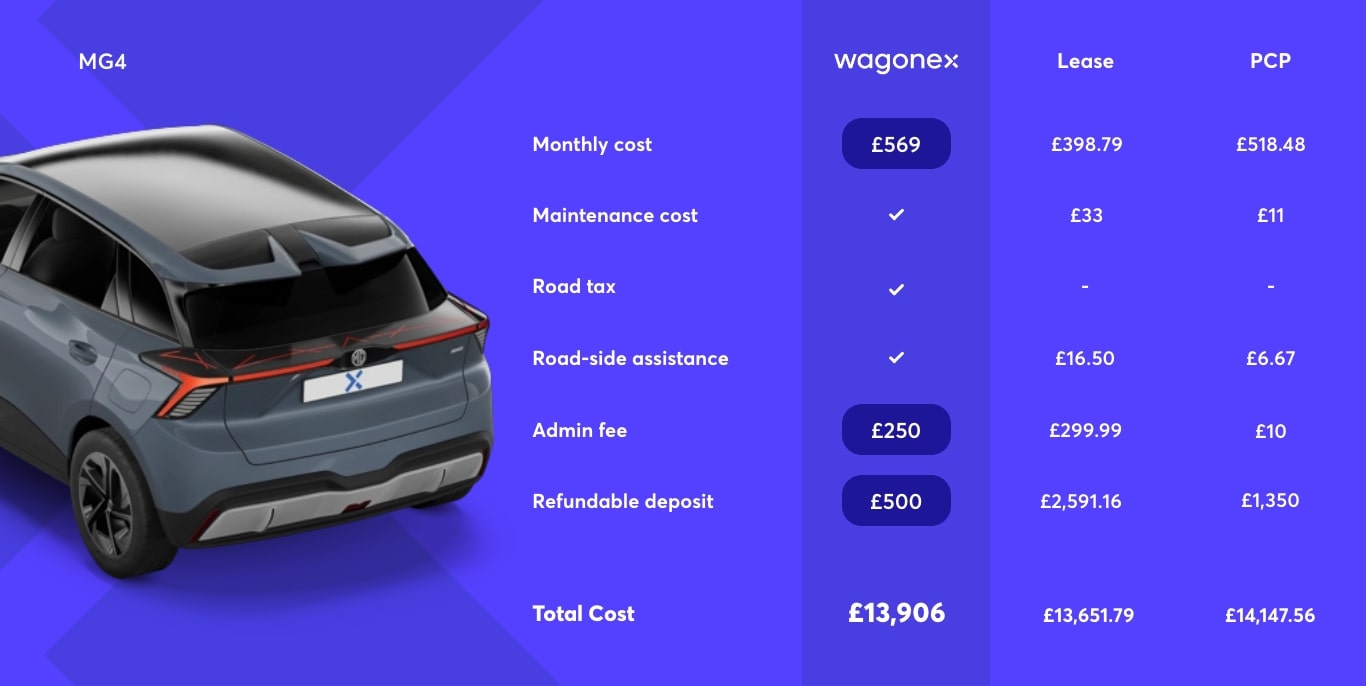

We’ve picked 3 different kinds of car*, a Diesel (VW T-Roc), a hybrid (Mercedes-Benz GLA) and a full EV (MG4), to give you an idea of how the costs look for different fuel types.

The results are in, and Subscription comes out as the winner!

In 2 out of 3 examples, Subscription has the cheapest costs for a 24 month deal, and is only slightly more expensive than Leasing in the MG4 case. Choosing a Subscription over PCP could save you more than £5k on some cars, which is unbelievable!

Whilst we’re on the topic of costs, another cost to think about is the premium you pay for Subscription’s flexibility. You might think “You told me I could get shorter term Subscriptions, but I bet you have to pay over the odds for that privilege”.

Yes, it’s true that you might pay a premium for a 1 month or 3 month contract, but if you look at Subscription costs for 12 month contracts you actually pay little or no premium at all, it all depends on the supplier!

You can see that for the T-Roc and MG4, with some of our suppliers you don’t actually pay any extra for taking out a 12 month subscription vs a 24 month one. So, more freedom at no extra cost. And even with the GLA, you only pay £12 a month more for the freedom of a 12 month contract vs the 24 month contract.

Summary

To summarise, Car Subscription can work out a cheaper and more flexible way to get a new car, once you factor in the total cost of ownership.

Subscription offers unparalleled flexibility with contract length. It’s super convenient and you don’t need to put down your hard earned savings upfront; the deposit you do pay is refundable when you return the car!

So with all that in mind, it begs the question; why wouldn’t you choose Subscription for your next car?

Follow this link to browse our full list of cars available for subscription.

* Prices correct at time of writing